Imagine flipping the calendar to March. Other business owners are casually handing over neatly organized, perfectly reconciled files to their CPAs. Whereas, you are staring at a mountain of unopened bank statements, a chaotic digital drive, and a physical shoebox stuffed with fading receipts. That sinking feeling in your gut is entirely real.

The sheer weight of months (or perhaps even years) of unrecorded, messy transactions can absolutely paralyze a business owner. But here is the good news. The path from total financial chaos to pristine, tax-ready accounts is completely achievable. It all starts with a targeted financial rescue mission known as catchup bookkeeping.

Catch-up Bookkeeping is the methodical, highly detailed process of dragging your historical financial records into the present.

Every single dollar that moved through your business must be accounted for. It gets properly categorized. It gets flawlessly reconciled. By doing this, you transition from a state of reactive stress to absolute proactive financial control.

Let’s break down exactly how this restorative accounting process works, why your business survival depends on it, and the undeniable signs that it is time to call in the professionals.

What Exactly Is Bookkeeping Catch Up?

In the unforgiving world of business accounting, a “backlog” is not merely an annoying administrative to-do list you can push off until next week. It is a massive, ticking liability. Leaving your books unattended creates a rapid snowball effect of unreconciled bank feeds, missing vendor receipts, and uncategorized expenses that severely distort your true financial reality.

So, what is catch-up bookkeeping in a practical, day-to-day sense? It involves diving headfirst into that neglected backlog to untangle the mess. We are talking about forensically reviewing past months to find out exactly where every cent went. This means hunting down missing invoices, identifying duplicate charges, re-classifying miscoded assets, and aligning your software with actual bank truth.

Is It The Same As Standard Accounting?

People often confuse this with standard accounting. They are fundamentally different beasts. Regular monthly bookkeeping is about routine maintenance. It keeps your real-time records humming along smoothly, assuming the historical data is already correct. Restorative services, however, look backward. They fix broken data, fill in gaping historical holes, and ensure your financial foundation is rock solid before you build on it.

Think of it as a deep, structural restoration for your business’s financial engine. You can’t tune a car that has a blown transmission, and you certainly can’t run accurate financial projections on books that are six months behind.

To make the distinction crystal clear, here is how the two compare:

| Feature | Regular Monthly Bookkeeping | Catch-Up Bookkeeping |

| Primary Goal | Maintain current financial health and real-time reporting. | Restore historical accuracy and fix accumulated errors. |

| Time Focus | Present (Current month transactions). | Past (Months or even years of backlogged data). |

| Work Volume | Predictable, steady workflow month-to-month. | Heavy, intensive, forensic data auditing. |

| Common Tasks | Weekly categorizing, monthly reconciliations, payroll entry. | Hunting missing statements, untangling commingled funds, rebuilding the chart of accounts. |

| The End Result | Up-to-date, consistent financial tracking. | A clean slate that allows normal bookkeeping to safely resume. |

Why Your Business Can’t Ignore Overdue Books (Key Benefits)

Letting your financial records gather dust doesn’t just trigger personal anxiety. It actively drains your bank account. Ignoring the problem inevitably leads to compounding accounting errors, severe IRS penalties, and missed growth opportunities. By actively bringing in trusted accounting experts, you unlock several non-negotiable benefits that protect your bottom line.

Maximizing Tax Compliance & Bulletproof Deductions

The golden rule of the IRS is brutally simple: you cannot claim what you haven’t meticulously recorded. Every missed receipt is literal money out of your pocket. By updating your ledger, you capture every single legitimate tax write-off.

We aren’t just talking about major equipment purchases. This includes fractional mileage, obscure travel expenses, merchant gateway fees, and those endless software subscriptions you forgot you were paying for. Proper Catch-up Bookkeeping for Businesses ensures you stop overpaying the government and start keeping the capital you rightfully earned.

Unlocking Loan & Funding Readiness

Cash flow crunches happen to the best of us. When they do, you might urgently need a line of credit, an SBA loan, or investor capital to bridge the gap. The very first thing a bank or private investor will demand is a pristine, up-to-date Balance Sheet and a current Profit & Loss (P&L) statement.

If you hand an underwriter a P&L from eight months ago, they will show you the door immediately. Behind-schedule books effectively signal to lenders that your business is a high-risk gamble. Clean books prove you run a tight, disciplined operation.

Securing Accurate Financial Insights

You simply cannot steer a ship if your navigation system is fundamentally broken. Operating on outdated financial data means you are flying blind in a competitive market. Are your profit margins suddenly shrinking because material costs spiked last quarter? Are you actually losing money on a specific service tier that you thought was profitable?

You won’t know the truth until the data is current. Updated ledgers provide an unvarnished, factual look at your true profit versus loss. This empowers you to make aggressive, data-driven decisions rather than relying on gut feelings and outdated assumptions.

Reclaiming Your Peace of Mind

Do not underestimate the heavy mental toll of tax-related stress. Waking up at 3 AM wondering if you are going to get audited, or sweating over how you will explain the mess to your CPA, is no way to run a company.

Getting your books current eradicates that heavy mental burden. Once Outsourced Accountants steps in and clears the backlog, you can finally breathe. It allows you to redirect your mental energy toward revenue-generating activities, client acquisition, and scaling your operations.

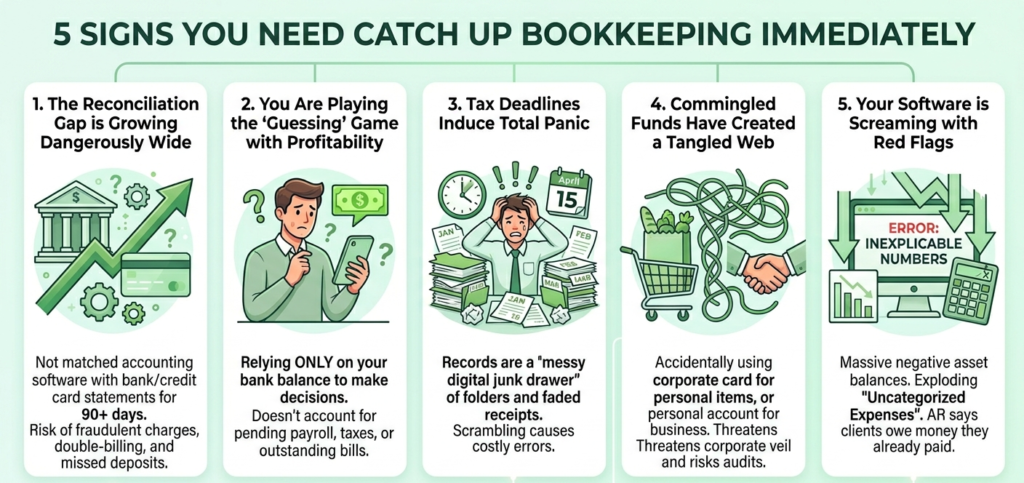

5 Signs You Need Catch Up Bookkeeping Immediately

Business owners rarely fall behind on purpose. It happens by slow degrees. You get incredibly busy closing deals, handling daily client emergencies, putting out operational fires, and suddenly, a whole quarter has slipped by without a single bank reconciliation.

Not sure if your specific situation warrants a professional financial intervention? If any of these five red flags are waving in your day-to-day operations, it is time to seriously prioritize catch up bookkeeping before the financial damage multiplies.

1. The Reconciliation Gap is Growing Dangerously Wide

If you haven’t matched your accounting software transactions against your actual external bank and credit card statements in 90 days or more, you are officially in the danger zone. Reconciliation is not optional. It is the only guaranteed way to catch fraudulent charges, double-billing from vendors, or missed deposits that never actually cleared the bank. Leaving this undone is the financial equivalent of leaving your business’s front door wide open overnight.

2. You Are Playing the “Guessing” Game with Profitability

Are you logging into your mobile banking app, staring at the available balance, and using that number to decide if you can afford to hire a new employee or buy new inventory? That is a massive operational mistake. Your bank balance tells you absolutely nothing about pending payroll runs, upcoming quarterly tax liabilities, or outstanding net-30 vendor bills. If your raw bank balance is your only financial compass, you desperately need Startup Catch-up Bookkeeping to establish real, accrual-based reporting.

3. Tax Deadlines Induce Total Panic

When Q4 officially ends, you should feel a profound sense of accomplishment for surviving another year in business. Instead, you feel pure, unadulterated dread. Your “records” currently consist of a messy digital junk drawer on your desktop and physical folders jammed with faded, crumpled invoices. Scrambling to organize this in March guarantees costly errors. You need a systematic clean-up well before your CPA starts asking for your finalized files.

4. Commingled Funds Have Created a Tangled Web

It happens. You accidentally use the corporate card for a personal grocery run, or worse, you pay a business vendor directly from your personal checking account because the primary business account was running low. Doing this once or twice is a headache; doing it for six months creates an absolute nightmare for tax preparation. Untangling commingled funds requires extreme precision to preserve your corporate veil and avoid terrifying personal tax liabilities. Professional catch-up bookkeeping is the only safe way to separate the mess without triggering an audit.

5. Your Software is Screaming with Red Flags

You finally log into Xero or QuickBooks and see terrifying, inexplicable numbers. You have a massive negative balance in your asset accounts, or an exploding “Uncategorized Expenses” bucket that totals tens of thousands of dollars. Maybe your Accounts Receivable report shows that clients owe you $50,000, but you know for a fact they already paid you months ago. These software anomalies do not just fix themselves over time. They require a forensic eye to trace the localized errors back to their exact origin and correct them permanently.

This is exactly where bookkeeping for small businesses saves the day. Specialists don’t just delete the bad numbers; they repair the broken workflows so the software actually serves you again. Whether it’s a massive inventory discrepancy requiring an Ecommerce Catch up Bookkeeper or a local service business with messy payroll entries, fixing the root cause is the only way forward.

Let Our Experts Handle Your Catchup Bookkeeping Needs Today

The Step-by-Step Process: How Catching Up Works

When you finally wave the white flag and hand over a messy ledger to professional Outsourced Accountants, the rescue operation doesn’t happen by magic. It requires a highly structured, surgical approach to ensure absolutely nothing falls through the cracks. Financial restoration is an exact science.

Here is the exact blueprint of how we pull your business back from the brink of accounting chaos and establish perfectly balanced books:

Phase 1: Comprehensive Data Collection (The Fact-Finding Mission)

Before any numbers can be crunched, we need the raw materials. This is often the most daunting part for business owners, but an expert team makes it painless. We gather every single necessary financial document for the missing periods.

● Bank and Credit Card Statements

We pull the official PDF statements, not just the raw CSV data, to ensure we are matching against the bank’s definitive record.

● Payroll Reports

We collect all historical payroll runs from your provider (like Gusto, ADP, or Paychex) to properly allocate gross wages, employer taxes, and benefit deductions.

● Loan Documents and Amortization Schedules

If you bought a company vehicle or took out an SBA loan during the blackout period, we need the origination documents to split the principal and interest payments correctly.

● Point of Sale (POS) Reports

For retail or service businesses, we pull the gross sales and merchant fee data from Stripe, Square, or Shopify.

Phase 2: Forensic Categorization (Fixing the Chart of Accounts)

Once the raw data is centralized, the heavy lifting begins. If you have ever looked at your bank feed and seen Amazon listed 40 times with no context, you know how tedious this is. Every single historical transaction must be painstakingly investigated and mapped to the correct category within your Chart of Accounts.

Did that Home Depot run include office supplies (a standard expense) or a massive piece of equipment (a fixed asset that needs to be depreciated over time)? Was that dinner a 50% deductible client meal, or a 100% deductible company-wide party? Getting these classifications perfectly aligned is what ultimately maximizes your tax write-offs and protects you during an IRS audit.

Phase 3: The Ironclad Reconciliation (Finding the Missing Pennies)

This is where the amateur bookkeepers fail and the trusted accounting experts shine. Reconciliation is the act of comparing your internal accounting software (like Xero) against your external bank records. The ending balances must match identically, right down to the exact penny.

If your bank statement says you ended May with $42,516.33, but QuickBooks says you had $40,000.00, we hunt down that missing $2,516.33. This process uncovers uncashed checks you wrote to vendors, customer payments that bounced, or accidental double-entries that are artificially inflating your expenses.

Phase 4: Financial Reporting (The Final Delivery)

Once the data is scrubbed, categorized, and reconciled, the fog officially lifts. We don’t just hand you a login and say “good luck.” We generate and analyze the definitive financial reports that tell the true story of your business:

● The Trial Balance

Proving that your total debits perfectly equal your total credits.

● The Income Statement (P&L)

Revealing exactly how much money you actually made (or lost) after all hidden costs are factored in.

● The Balance Sheet

Showcasing your current business net worth, detailing your liquid assets against your outstanding liabilities.

| Process Phase | What Happens | Why It Matters |

| 1. Data Collection | Aggregating bank, POS, and payroll statements. | Ensures no transaction is left behind or guessed at. |

| 2. Categorization | Mapping expenses to the Chart of Accounts. | Maximizes legal tax deductions and prevents audit triggers. |

| 3. Reconciliation | Matching internal software to external bank data. | Catches fraud, duplicate entries, and missing deposits. |

| 4. Reporting | Generating the Balance Sheet and P&L. | Delivers actionable intelligence for business growth. |

DIY vs. Professional Catch-Up Services

Let’s be brutally honest. Catch up Bookkeeping for small business is not really a big problem. However, as an entrepreneur, your natural instinct is to roll up your sleeves, brew a massive pot of coffee, and try to “power through” the backlog yourself on a Sunday afternoon. You assume you can just quickly accept all the transactions in your bank feed and be done with it.

This is a catastrophic trap. Fixing months of compounded financial errors is exponentially harder than doing the bookkeeping correctly the first time.

When untrained users attempt a massive historical cleanup, they often resort to the accounting equivalent of “keyword stuffing,” forcing numbers into random categories just to make the red alerts go away. They dump massive, unexplained sums into “Miscellaneous Expenses” or “Ask My Accountant,” which is an immediate, glaring red flag for an IRS auditor. DIY attempts frequently lead to duplicated revenue entries (making it look like you made way more money than you did, causing you to overpay taxes) or miscategorized fixed assets.

The sheer time-saving value of hiring a dedicated specialist cannot be overstated. Your time as a founder is incredibly valuable. If your effective hourly rate as a CEO is $150 an hour, and you spend 40 hours fumbling through Xero to fix eight months of bad data, you just cost your company $6,000 in lost productivity and revenue-generating activities.

Professionals have enterprise-level tools to automate bulk data entry safely. They understand the complex mechanics of journal entries. Most importantly, they possess the trained, analytical expertise to spot weird historical inconsistencies that the untrained eye would completely ignore. You wouldn’t perform DIY electrical work on your commercial office building; do not perform DIY forensic accounting on your livelihood.

Conclusion

Letting your financial records slip into chaos is a common business mistake, but leaving them there is a fatal one. Catch-up bookkeeping isn’t just about dwelling on the mistakes of the past; it is a strategic maneuver designed entirely to secure your business’s future.

Whether you are a rapidly scaling agency desperately needing pristine investor reports, or a local contractor simply trying to survive the impending tax season without a panic attack, the ultimate goal remains exactly the same: total financial clarity. You cannot scale a business built on a foundation of “Uncategorized” transactions and guesswork.

Don’t let another month of financial anxiety hold your growth hostage. Stop guessing what your profit margins are, and stop dreading the inevitable call from your CPA. Reach out to the experts at Outsourced Accountants today to schedule a comprehensive “Bookkeeping Health Check.” Let us do the heavy lifting to turn your historical financial chaos into a pristine, actionable roadmap for long-term success.

Frequently Asked Question

What is the main goal of bookkeeping restoration?

The primary objective is to forensically convert unorganized, neglected, and highly complex financial data into perfectly accurate, actionable, and fully tax-ready reporting. It restores trust in your numbers.

Do I need to stop current operations to catch up?

Not at all. This is a common misconception. A professional accounting service will securely pull your historical data and work on untangling the past in the background, allowing you to seamlessly continue running your daily business operations without interruption.

Is it ever “too late” to catch up?

It is quite literally never too late to fix your books. However, the absolute truth is that the sooner you act, the easier and less expensive the process will be. Delaying only makes retrieving missing documentation and old bank statements increasingly difficult. Start the rescue process today.

How long does catch-up bookkeeping take?

There is no one-size-fits-all answer, as the timeline is entirely dependent on the severity of the backlog. Generally speaking, a minor cleanup involving three to six months of straightforward data can often be finalized and delivered within one to two weeks. However, multi-year historical restorations can take a full 30 to 45 days of intensive forensic work.

Is catch-up bookkeeping expensive?

Cost is relative. Yes, there is an upfront investment for the highly intensive, specialized labor involved in untangling a financial disaster. Because it is project-based forensic work, it costs more than a standard monthly bookkeeping retainer. However, you must weigh that upfront cost against the alternatives.

Can I use QuickBooks for catching up?

Absolutely. Industry-standard platforms like QuickBooks Online and Xero are excellent ecosystems for housing your restored data. However, they are just tools. A hammer doesn’t build a house on its own. Bringing a dead QuickBooks file back to life requires a highly skilled hand.